“As weaker companies fall away, that leads to greater opportunities for those that are strong and can really step up their market share to succeed in the future.”—Guy Anderson

- UK stocks are trading at attractive valuations due to the uncertainty over Brexit and Covid.

- The Mercantile Investment Trust is positioned to capture disruption from these challenges as well as upside when the uncertainty clears and the economy rebounds.

- The portfolio’s gearing is high relative to history, reflecting the opportunities we see.

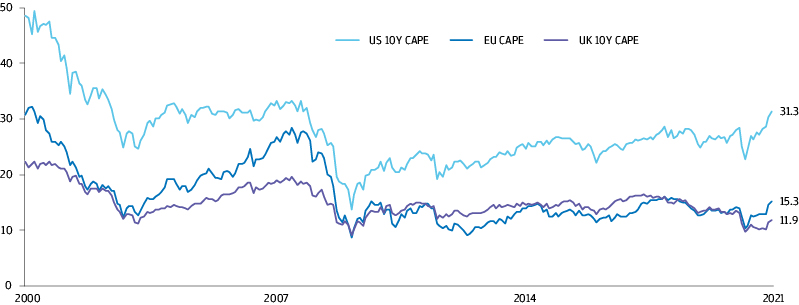

UK stocks look cheap compared to the US and European markets

Source: Panmure Gordon Research. Data as of 8 January 2021. CAPE is the cyclically adjusted price-to-earnings ratio.

The valuations of UK stocks are reflecting the uncertainty surrounding both Brexit and Covid-19, and the many related economic impacts. The mid- and small-cap universe is full of companies with sound business models and strong prospects — even in the face of these challenges — that are now trading at discounted valuations. We are taking advantage of this opportunity to position the portfolio with these quality companies that will benefit in an eventual recovery or that may already be benefiting from new and disruptive trends.

Positioning in the portfolio reflects the dynamic environment and the potential for both cyclical and Covid-19 economic recoveries. The portfolio is also well-exposed to new or disruptive trends, particularly from Covid-19. For example, retailers with a strong digital presence have actually thrived during the pandemic as people have been forced to shop online, while those with weak online capabilities have suffered greatly as high streets are shuttered.

The pandemic actually propelled the growth of a number of markets. In addition to the accelerated growth of a wide variety of online services – from education to healthcare – some markets, such as suburban and country properties, have grown significantly as citydwellers sought outdoor space and room for a home office.

Similarly, pet ownership has risen dramatically as people have spent much more time at home. Pets typically live longer than 10 years so the market for pet care products and veterinary services is on track for rapid growth over the next decade. The commitment to pet ownership increases the stability and visibility of this trend – this stands in contrast to some recent growth trends, such as working from home, which may or may not normalise.

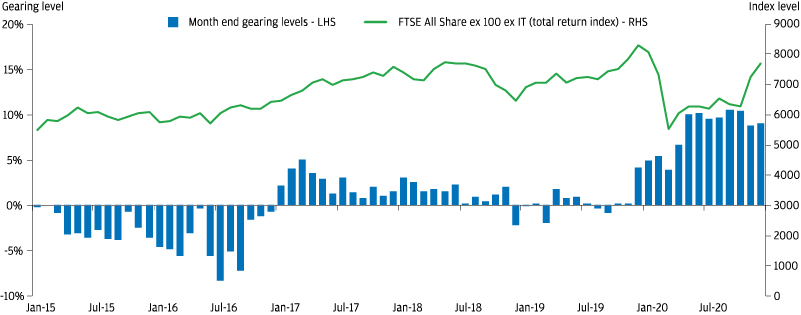

Gearing in the portfolio is elevated relative to history, reflecting the many opportunities

Source: Bloomberg, J.P. Morgan Asset Management. As at 31 December 2020 (weightings exclude cash/cash equivalents).

Gearing allows an investment trust to borrow money that can be used to take advantage of timely investment opportunities without having to sell existing assets to raise funds; it aims to boost the gains made by a trust as the value of its portfolio companies rise. However, investors should be aware of the other side of the equation—gearing will mean that losses incurred in a falling markets will also be magnified.

For this reason, the portfolio manager of the Mercantile Investment Trust has been an active manager of gearing levels, varying the levels of net borrowing to match the risks and rewards offered in particular market environments. Gearing levels are increased in the expectation of market growth and are reduced – often to below zero, meaning the Trust has a net cash holding – when the outlook is uncertain or the portfolio managers are less sanguine about future prospects.

Since mid-2020, gearing in the trust has been about 10%, the highest level for a number of years. This reflects the portfolio manager’s current assessment of the opportunities presented by the market: attractive valuation levels are now combined with strong growth potential offered by companies in the portfolio.