“The most interesting thing about operating in the mid- and small-cap part of the market is that we can see these new opportunities when they arise, when the businesses are young and are experiencing that supernormal growth.” –Guy Anderson

- UK mid- and small-cap companies have generated some of the best long-term returns in the world.

- They tend to be faster growing and more exposed to future growth drivers.

- Other benefits of the asset class include significantly more exposure to the domestic economy than the FTSE 100 and more potential to generate alpha due to less analyst coverage.

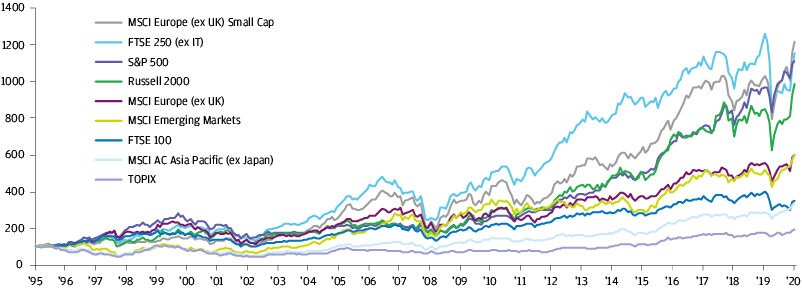

Long-term returns of smaller UK companies beat the FTSE 100—and many other markets

Source: J.P. Morgan Asset Management, Bloomberg. All series are rebased to 100 as at 31 October 1995 to 31 December 2020. All indices in GBP and include reinvested dividends. Indices do not include fees or operating expenses and are not available for actual investment. Past performance is not a reliable indicator of current and future results.

Faster growth and exposure to future growth trends should continue to drive strong performance of UK mid- and small-cap stocks going forward. These companies tend to have at least one of the following three characteristics:

- Nimble business models: the ability to pivot quickly depending on business conditions helps companies survive challenging times and take share from less flexible competitors. Mid- and small-sized companies tend to have a less bureaucratic decision-making process, fewer geographic locations to manage and a less complex supply chain.

- Innovative or disruptive: many mid- and small-cap companies have developed a new product, service or business model that is capable of disrupting an existing way of doing business or an entire industry. Since the turn of the century we’ve seen enormous changes across many industries – traditional retailers have been disrupted by the shift to online shopping while traditional forms of communication have been disrupted by social media.

- Exposure to rapidly growing new markets: some companies are capable of fast growth because they are exposed to a new or rapidly growing market, from country properties to online gaming to pet care products.

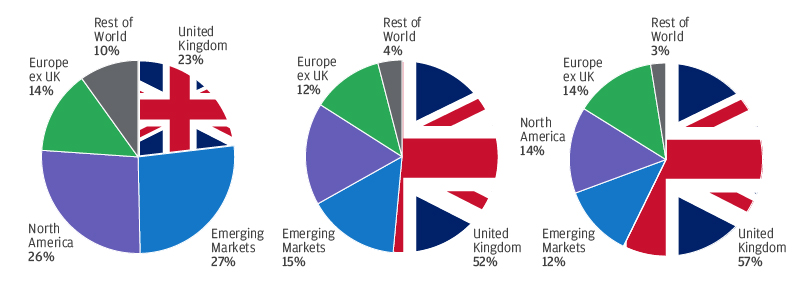

Mid- and small-cap UK stocks offer much more exposure to domestic growth than the FTSE 100

Source: J.P. Morgan Asset Management

The natural increase in domestic exposure from mid- and small-cap UK companies could be advantageous in the current environment, with concerns over Brexit subsiding and the potential for an economic rebound as the vaccine rollout progresses.

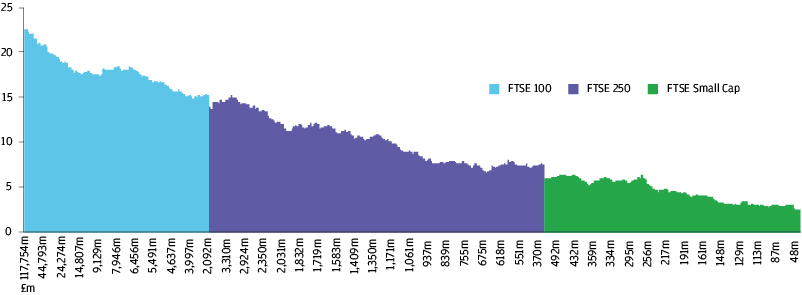

Less research coverage of mid- and small-cap stocks can increase the potential for earnings surprises and outperformance (or underperformance)

Average 18 analysts covering each FTSE 100 company and 10 analysts covering each FTSE 250 company. Sources: Liberum, Datastream as of 11 January 2021

Fewer analysts covering mid- and small-cap companies can lead to a greater variation in earnings estimates and other metrics used to assess a company’s fundamentals. This can increase the potential for a company to beat (or miss) earnings estimates and for its stock to out- or underperform, creating more opportunities for active portfolio managers to generate alpha.